Uncertain firm profits and (indirectly) priced idiosyncratic volatility

University of Oklahoma, Monash University and University of Iowa – Department of Finance

Xuhui (Nick) Pan, Bharat Raj Parajuli and Petra Sinagl

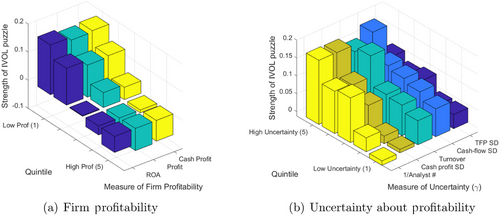

Abstract: We show that the negative relation between idiosyncratic volatility (IVOL) and expected returns exists only among firms with low profitability and high uncertainty about profitability. We propose an incomplete information model in which agents cannot disentangle systematic from idiosyncratic shocks. While not priced directly, IVOL affects expected re- turns by lowering signal accuracy, which decreases the factor loading on the priced systematic risk and yields the negative IVOL-return relation. The model predicts that this negative relation is the strongest among underperforming firms with highly uncertain profitability. When applied to U.S. equity data, we explain 86% of the negative IVOL-return relation.

Price Inefficiency Specific to Firm-Specific Information and Anomalies

Monash University

Abstract: I develop an instantaneous aspect of price inefficiency of firm-specific information (IPIFI) measure and examine its relation with 210 anomalies. IPIFI captures the speed at which prices incorporate the left-over firm-specific information not incorporated into prices contemporaneously. In Fama-MacBeth regressions, IPIFI interaction term takes away the statistical significance of consolidate anomalies. IPIFI is high when firm-specific information is difficult to interpret; a firm produces more price-relevant event news; and fundamental uncertainty is high. The results suggest that, on average, market anomalies primarily exist where IPIFI is high.

Economic Benefits of Firms’ Government Sale Dependency

Monash University

Abstract: In this paper, using a new channel of political connections, firm dependency on government sales, I study the value of political connections for firms. I find an economically and statistically significant relation between firm dependency on government entities in terms of revenues and the cross-section of future stock returns. Firms experience significantly higher profit margins post government dependency. In addition, past government sales significantly predict future government sales. The atypical features of government contracts and the information asymmetry between the contractor and contractee are likely to be behind the firms’ higher profit margins. Further tests based on attention and uncertainty proxies suggest that investors’ limited attention and greater valuation uncertainty contribute to abnormal returns. Furthermore, I find evidence suggesting that firms gain the wealth effects of political connections found by Cooper, Gulen, and Ovtchinnikov (2010) by winning material government contracts; however, the wealth effects of government dependency stay strong even after controlling for such connections.

ESG Everywhere

Monash University, University of Utah – David Eccles School of Business and University of Luxembourg

Bharat Raj Parajuli, Michael J. Cooper and Michael Halling

Abstract: Our findings reveal that ESG is everywhere in mutual fund investment decisions-playing an important role not only for ESG-designated funds but across all categories of mutual funds-ranking ahead of traditional factors such as momentum and book-to-market ratios. Surprisingly, ESG scores matter for all funds even in the most recent data, a period of arguably anti-ESG sentiment. We find that ESG scores have an even greater impact in brown industries, such as oil and gas, than in non-brown industries and for mutual fund managers with Democratic party leanings. These results highlight the evolving priorities of mutual fund managers, with ESG considerations increasingly integrated into investment strategies alongside traditional risk-return metrics.

Is Positive Information more Valuable to Investors than Negative Information?

Monash University

Abstract: I motivate and find empirical evidence that positive information is more valuable to investors than negative information. Post corporate under-(over-)valuation signals, information production increases (decreases), increasing (decreasing) price informativeness (PI). PI decreases more in firms with worse investment opportunities, poor corporate governance, more entrenched manager, and higher short-sale constraints. And, PI increases more in firms with better investment opportunities and higher investment-to-Q ratios. Results imply that market over-valuations are corrected slower than under-valuations and hence are stickier and more prevalent in the economy. Persistent and long-lasting performances of short-legs of anomaly portfolios could be the result of such a phenomenon.