Asset Pricing Implications of Firms’ Government Sales Dependency

Abstract: This paper investigates the firm-level, asset pricing implications of government expenditures. Higher government sales dependency (GD), unconditional on political partisanship cycles, significantly predicts positive future returns, and a GD-weighted portfolio substantially improves the tangency portfolio’s ex post Sharpe ratio. Conditionally, the results are stronger during Republican presidencies. Higher returns do not stem from political connections or political and regulatory risks. The underlying economic channel is higher expected cash flow from increased profitability. Atypical provisions of government contracts and information asymmetry likely drive higher profit margins. A risk versus a mispricing analysis elicits more convincing evidence for mispricing as an explanation for abnormal returns.

Firm Disclosures, Uncertain Profits, and (Indirectly) Priced Idiosyncratic Volatility

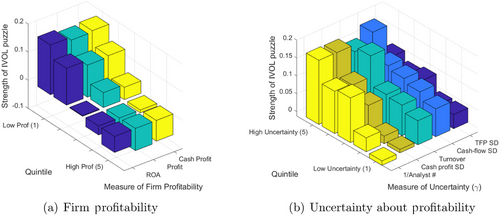

Abstract: We show that the negative relation between idiosyncratic volatility (IVOL) and expected returns exists only among firms with low profitability and high uncertainty about profitability. We propose an incomplete information model in which agents cannot disentangle systematic from idiosyncratic shocks. While not priced directly, IVOL affects expected returns by lowering signal accuracy, which decreases the factor loading on the systematic risk and yields the negative IVOL-return relation. The model predicts that this negative relation is the strongest among underperforming firms with highly uncertain profitability. Our model effectively explains a significant portion of the observed negative IVOL-return relation (86%) in the data.